Secular growth stocks have been dramatic relative underperformers for the last 11 months. This underperformance was quiet at first but has become really notable in 2021. The chart above shows that cheap consumer stocks as measured by the GS Consumer Cheap basket have outperformed expensive, secular growth technology stocks as measured by the GS TMT US High Growth basket by 114% since July 1, 2020. Secular growth stocks in the technology and consumer sectors are generally 30 to 50% off their 52-week highs, which combined with growth in their underlying fundamental financial metrics, make their valuations much more reasonable on both near term numbers and looking out 5 years. This is especially true relative to stocks in other industries that are up significantly since the Pfizer vaccine announcement and making all-time highs.

Much has been written about rising interest rates as the proximate cause for all of this and without opining on either causality or the future direction of rates, I will simply say that the market has digested a significant move in the 10-year from historically low levels. The market is also concerned about inflation. Similarly, I have no opinion on the future direction of inflation, but I would note that Warren Buffett’s fantastic article from 1977, “How Inflation Swindles the Equity Investor,” suggests that high ROE/ROIC businesses should outperform low ROE/ROIC businesses in a high inflation environment as they will suffer less relative compression in their ROEs and ROICs. Pricing power is also obviously important, but less important than relative ROIC/ROE. Technology companies broadly speaking have some of the highest ROICs in the market even if these unit economics are obscured by conscious decisions to invest in growth for some of the less mature businesses.

However, I think a much more important factor at work in the recent weakness of secular growth stocks than either interest rates or inflation lies in their name; i.e. the fact that they are “secular” and are therefore definitionally less GDP sensitive. This dynamic, combined with significant GDP declines in 2020 along with the happenstance fact that many of them benefitted from “Work From Home,” led to these stocks having the best fundamentals in the market last year on a relative basis. This was manifest in the fact that they had the most positive estimate revisions for their revenues, EBITDA and even occasionally EPS in the stock market. After having the best relative revisions in the market last year, these same dynamics have resulted in secular growth stocks having the worst relative sales, EBITDA, EPS and FCF revisions in the market in 2021 as GDP growth accelerated, which has driven significant positive sales and EPS revisions for cyclical stocks. Relative revisions drive relative performance over short 1 year time frames. Duration of growth and changes in ROIC drive relative performance over longer time frames.

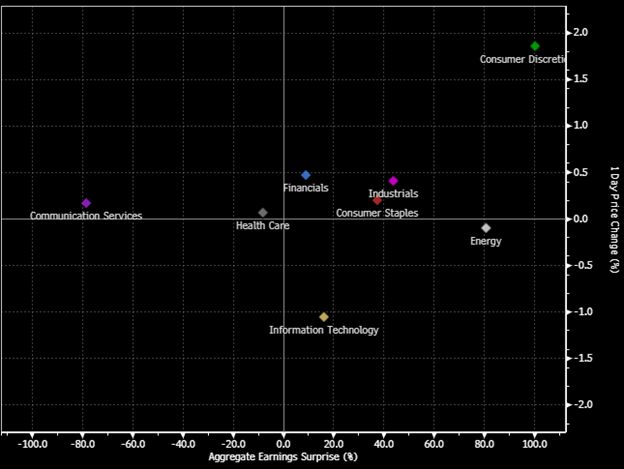

I think that the relative weakness in secular growth stocks fundamentals exemplified by their terrible relative revisions is nearing an end. For anyone confused who believes that the fundamentals of secular growth stocks have been good — yes, their fundamentals have been good in absolute terms, but the 10 to 20% beats seen in secular growth land this earnings season are actually disappointing relative to what has been happening in the rest of the market. The most recent poster child for this phenomenon is Dillard’s, which just reported a real $7.25 in quarterly EPS, which was a 500% beat vs. the $1.20 consensus. Even after going up ~40% in two days, it is still an optically cheap stock on run rate earnings which may or may not be durable but forward estimates are at least finally vaguely accurate. The chart below comparing earnings surprise to stock reaction shows this writ large.

Source: Bloomberg

I can’t speak authoritatively about the industrial, financial and/or energy sectors, but for the last 10 months the consumer sector was filled with stocks like Dillard’s where estimates were obviously wrong by massive amounts. Estimates for cyclical stocks in consumer finally seem to be in the right galaxy, although not yet the right solar system, after a string of dramatic upside surprises which means that revisions for these stocks should slow down even in a “Roaring 20s” scenario. A stabilization/end to the dramatic positive sales, EBITDA and EPS revisions seen in more cyclical stocks will thereby improve the relative revisions of “secular” growth stocks. This needs to happen for the relative performance and stock prices of “secular” growth stocks to stabilize.

I became optimistic that every vaccine was going to work last summer and was convinced that the combination of multiple successful vaccines and unprecedented stimulus was likely to lead to the fastest GDP growth in my lifetime in 2021. Although this type of top-down view is rare for me, I was a cautious believer in the “Roaring 20s” hypothesis for consumer behavior and GDP growth. As a result, for the last 10 months, I have had a bias towards GDP sensitive stocks that could be valued on earnings rather than EV/S. Especially apparel retailers where even a few months ago it was easy to find stocks with 2022/2021 revenue estimates that were significantly lower than 2019, which seemed way too low. Running more accurate 2021/2022 revenues through these models led to 2021/2022 EPS estimates that were multiples of consensus estimates given their high incremental margins. Beyond significant near-term (2021/2022) upside, many of these companies have permanently improved their business models during Covid by closing stores, renegotiating leases and pulling forward many years of eCommerce growth and investment along the lines of what I outlined in this Medium article and for Target specifically in my presentation to help raise money for the SOHN Hearts & Minds Investment Conference 2020 philanthropies.

I have had similar biases in technology, where I have tried to avoid recurring revenue business models which are definitionally not GDP sensitive and within technology my ordinal ranking has been semiconductors/Internet advertising/e-commerce > payments > software. Even within software, I have tried to avoid pure recurring revenue models and own business models with embedded payments or transactional revenue models to give them more GDP sensitivity. Even those software stocks proved to be painful to own.

All of this began to change for me in the big secular growth sell-off in late March and has changed more decisively for me in May as estimates finally look more reasonable in most of the more cyclical sectors of the market, secular growth stocks have declined 30%–50% and many cyclical stocks are up 3x–5x over the last 10 months. Relative revisions are stabilizing, and relative valuations are more attractive. Secular growth stocks are increasingly attractive to me, although I will continue to own most of my consumer cyclicals as well, given they are still quite cheap.

Positioning is also much cleaner now. Per data from Prime Brokers*, US L/S hedge fund net exposure to Large Cap Tech is now down to the 23rd percentile over the last 12 months (note: it’s been in the ~75th percentile since 2010). ETF flows show Tech is in the 1st percentile on a one-year basis (or the lowest out of all 11 sectors), while Growth is in the 0th percentile. By way of comparison, Financials sits in the 100th percentile, Industrials and Materials each in the 99th percentile, and Energy the 94th percentile. The same hedge funds and ETF buyers that had historically high net exposure levels to secular growth and technology names at their peak relative performance in the late summer now have much lower net exposures. Cleaner positioning, lower relative valuations and stabilizing relative revisions are positive for secular growth. The time to rotate to cheap cyclicals exposed to vaccines, reopening and accelerating GDP was roughly three quarters ago, not today. It’s easy to “Be greedy when others are fearful and fearful when others are greedy,” but much harder to actually do this.

I am also excited as I believe the relevance of the top-down, macro themes that have dominated the market for the last 15 months — Covid, then WFH, then vaccine/GDP sensitivity — are fading. I think there is going to be significant dispersion going forward within cheap consumer cyclicals, within cheap technology and within “secular” growth. Accurately identifying which new habits — WFH, working out at home rather than gyms, remote meetings rather than business travel, car ownership, the great migration out of cities, food delivery — that formed during Covid are durable vs. ephemeral is going to be essential. Accurately identifying which cheap consumer cyclicals permanently improved their business models such that they can sustainably grow off 2021 numbers vs. those which did not invest and improve their business models is going to be critical. This is all a relief to me after the top-down, thematic market of the last 15 months. I would note that I am almost always early, so if history is any guide, this is not the bottom for “secular” growth stocks, but I do believe secular growth stocks are steadily becoming more attractive.

* Thanks, Ashton — maybe I’ll finally be quoted in your weekly note, which has been a lifelong ambition of mine.

** Please note that I have tried to avoid using the word “value” but could not avoid “growth.” I think growth and value are absurd distinctions. Better to be a “make money” investor than either a “value” or “growth” investor.

*** EV SPACs are still mostly zero shots. They are not “secular” growth stocks. Moving away from silly concept stocks will also be healthy for the market.